GXO Logistics, Inc.

New ways of managing logistics

GXO Logistics, Inc. GXO 0.00%↑

GXO is a logistics company that was formerly part of XPO, one of the world's largest and best managed companies in the transportation and logistics industry.

Gxo may be one of the best logistics companies in the world and in fact is one of the largest in the world, recently the company was listed among the top 500 companies in the world.

Logistics is a highly competitive industry that seeks to change the way we distribute commerce, which is why I believe that GXO will be a high-growth and successful company in the coming years.

Gxo operates 906 facilities worldwide with a total of 195 million square feet, making it one of the largest logistics companies in the world.

Business model and context

Logistics is a fast changing industry, I mean that the speed of operations changes a lot over the years, the sector changes a lot and only those who provide a good service and generate value for their customers survive.

Logistics is very important in the economy and for companies as it facilitates operations by reducing costs and risks.

What the company does within its operations is to facilitate high value-added warehousing and distribution, order fulfillment, e-commerce, reverse logistics and other supply chain services that are differentiated by our ability to provide customized, technology-based solutions at scale.

To be a logistics company resistant to the crisis and competition it is necessary to have a diversified portfolio of customers and above all customers who are leaders in their sector (customers who are not very difficult to be bankrupt).

Another important aspect to be a successful logistics company is the efficiency and speed of the activities, and how to achieve this is very simple with technology.

Technology is very important for logistics centers and that is why GXO has robots and machines that facilitate the work of logistics and warehousing.

But the company stands out from its competitors because of its use of technology and not only has the hardware but also the software to make operations as efficient as possible.

managing the logistics of a food company is not the same as that of a clothing company, and in that sense the company customizes and adjusts to the needs of each client.

In some cases the seasonality of some sectors is very high and the company needs to act quickly, GXO facilitates this logistics operation at the lowest possible cost.

For example, up to 30% of consumer goods purchased online are returned and this generates higher volumes at certain times of the year. We have developed analytics that predict surges in demand using a combination of historical data and customer forecasts.

As an industry leader that invests substantially in technology, we have access to an immense amount of data, as well as analytical processing capabilities to capitalize on that data by incorporating our learnings into customer solutions. We believe that our ability to process and act upon data is a key competitive advantage and differentiator.

Another very important aspect is customer retention and GXO has contracts where they retain 90% of their customers.

These contracts that GXO has with other companies are multi-year contracts.

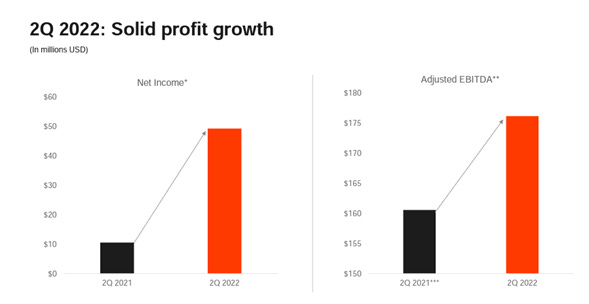

In its operations the company has grown in the last year thanks to new contracts, I believe that the company's growth potential is still very large and it can still gain market share.

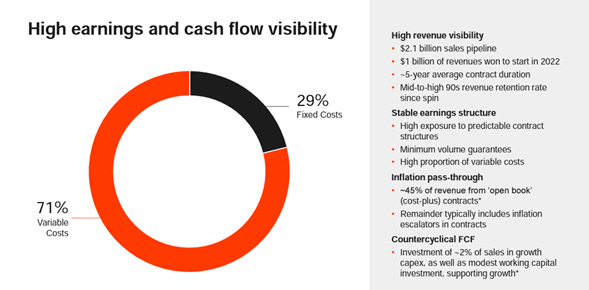

One may think that the company's profits may be affected by the cyclicality or change of trend in some sectors, but it is quite the opposite, the company has contracts where it stipulates the variation of costs in operations and can charge when something has a higher cost than planned.

The company is resilient and in inflationary environments like the current one where consumer confidence is lower and the economy is not growing as expected GXO can adjust its operations and not suffer in crises.

Debt

In July 2021, the Company completed an offering of $800 million aggregate principal amount of notes, consisting of $400 million of notes due 2026 (the “2026 Notes”) and $400 million of notes due 2031 (the “2031 Notes,” and together with the 2026 Notes, the “Notes”). The 2026 Notes bear interest at a rate of 1.65% per annum payable semiannually in arrears on January 15 and July 15 of each year, beginning January 15, 2022, and mature on July 15, 2026. The 2031 Notes bear interest at a rate of 2.65% per annum payable semiannually in arrears on January 15 and July 15 of each year, beginning January 15, 2022, and mature on July 15, 2031.

Investing Activities

Investing activities used $207 million of cash in 2021 compared with $280 million used in 2020. During 2021, we used $250 million of cash for capital expenditures, received $32 million in connection with the K + N acquisition and received $11 million from sales of property and equipment. During 2020, we used $222 million of cash for capital expenditures, used $40 million, net, in connection with the purchase and sale of affiliate trade receivables and used $30 million in connection with a pre-acquisition deposit for the K + N acquisition. During 2020, we received $12 million from sales of property and equipment.

Financing Activities

Financing activities used $241 million of cash in 2021 and generated $67 million of cash in 2020. The primary uses of cash from financing activities in 2021 were $774 million of net transfers to XPO in connection with the Separation, $128 million to purchase the remaining noncontrolling interest in GXO Logistics Europe SAS that we did not own, $72 million cash used to repay debt and finance leases and $26 million to repay borrowings related to our securitization program. The source of cash from financing activities in 2021 was the issuance of long-term debt of $794 million. By comparison, the primary sources of cash from financing activities in 2020 were $168 million of net transfers from XPO and $24 million from net borrowings related to our securitization program. The primary uses of cash from financing activities in 2020 were $123 million used to repay debt and finance leases and $21 million to purchase noncontrolling interests in GXO Logistics Europe SAS.

The company's management comes from XPO and I have to highlight the sincerity with which they speak in interviews and 10-Q of the company.

I learned about XPO from other investors and they emphasize the sincerity of the company and how the culture of the company is something that can also be seen in GXO and how they deal with every question in their calls and interviews.

It is a relatively new company with an over valuation after its spni-off but is now at a more attractive price to invest in.

The business model and valuation of the company at 17x P/E and 10X EBITDA are very attractive.

If the company continues with this business model it can continue to grow between 8-10% and generate about $1.2B of EBITDA for the next few years which would mean valuing at double what it is today at about $100 per share.